How CPF Accrued Interest Quietly Eats Your Profit.

You've held your property for years. The market has moved in your favour. Then your lawyer sends you the completion statement — and after paying off the mortgage and returning CPF funds plus accrued interest, the cash you receive is far less than expected.

This is one of the most common shocks I see sellers face. And almost all of it comes down to one thing: CPF accrued interest.

What Is CPF Accrued Interest?

When you withdraw CPF funds for property, those funds stop earning interest in your OA. But the CPF Board tracks what they would have earned at 2.5% per annum, compounded annually — and when you sell, you must refund both the principal and that accumulated theoretical interest.

The refund goes back into your CPF account, not your bank account. Only after that is settled do you receive your net cash proceeds.

The Numbers Are Bigger Than You Think

2.5% sounds modest. Compounded over 15–20 years, it isn't.

HDB flat, held 15 years:

If your net proceeds after clearing the mortgage are $320,000, you walk away with roughly $34,600 in cash — even if on paper it looked like a $120,000 gain.

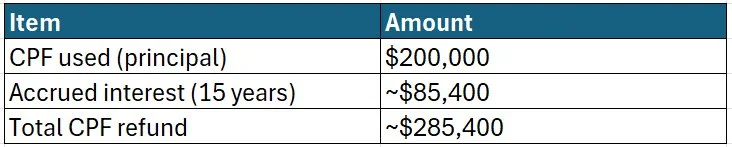

For a private property with $400,000 of CPF used over 20 years, the accrued interest alone can exceed $256,000. That's a quarter of a million dollars going back into CPF, not your pocket.

Check How Much is Your CPF Accrued Interest Here

| Year | CPF Used (Cumul.) | Interest This Year | Total Accrued Int. | Total to Return |

|---|

This calculator provides estimates for educational purposes only and does not constitute financial advice.

Figures are based on CPF OA interest rate of 2.5% p.a. compounded monthly. Actual amounts may differ.

Please verify with CPF Board (www.cpf.gov.sg) or your mortgage advisor.

The Biggest Misconception: "It Goes Back to Me, So It's Fine"

Technically yes — but CPF and cash are not the same thing. You cannot freely spend what's locked back in your OA. For upgraders, this is critical: your ABSD, cash-over-valuation, and renovation costs for the next property require real, accessible cash — not CPF that's just been refunded.

I've seen upgraders assume they have $200,000 in hand from an HDB sale, only to find their actual cash position is closer to $60,000 after the CPF refund. That changes everything about what they can afford next.

What You Can Do

You can't eliminate accrued interest, but you can plan around it.

Model your exit before you enter. When buying, estimate the accrued interest at your likely selling horizon. This sets your true break-even price — not just what covers the mortgage.

Don't anchor on the paper gain. Your real profit is what's left after clearing the mortgage, refunding CPF principal and interest, agent commissions, and legal fees. Always work from net cash proceeds.

Run the numbers early. The CPF Board's calculator at cpf.gov.sg lets you estimate what you'll owe. Do this before you commit to selling — or upgrading.

The Bottom Line

CPF accrued interest isn't a penalty. It's simply the invisible cost of using your retirement savings for property — one that stays hidden until the moment you sell.

Go in with eyes open. Model your exit before you enter. And if you'd like help running the numbers on your current property, reach out — it's exactly what I do.